With that said, we believe there are fundamental problems with gold, oil, and the U.S. dollar as stores of value going forward. Below, we will make the case that bitcoin is ultimately the only long-term protection against inflation.

– The Case for $500K Bitcoin

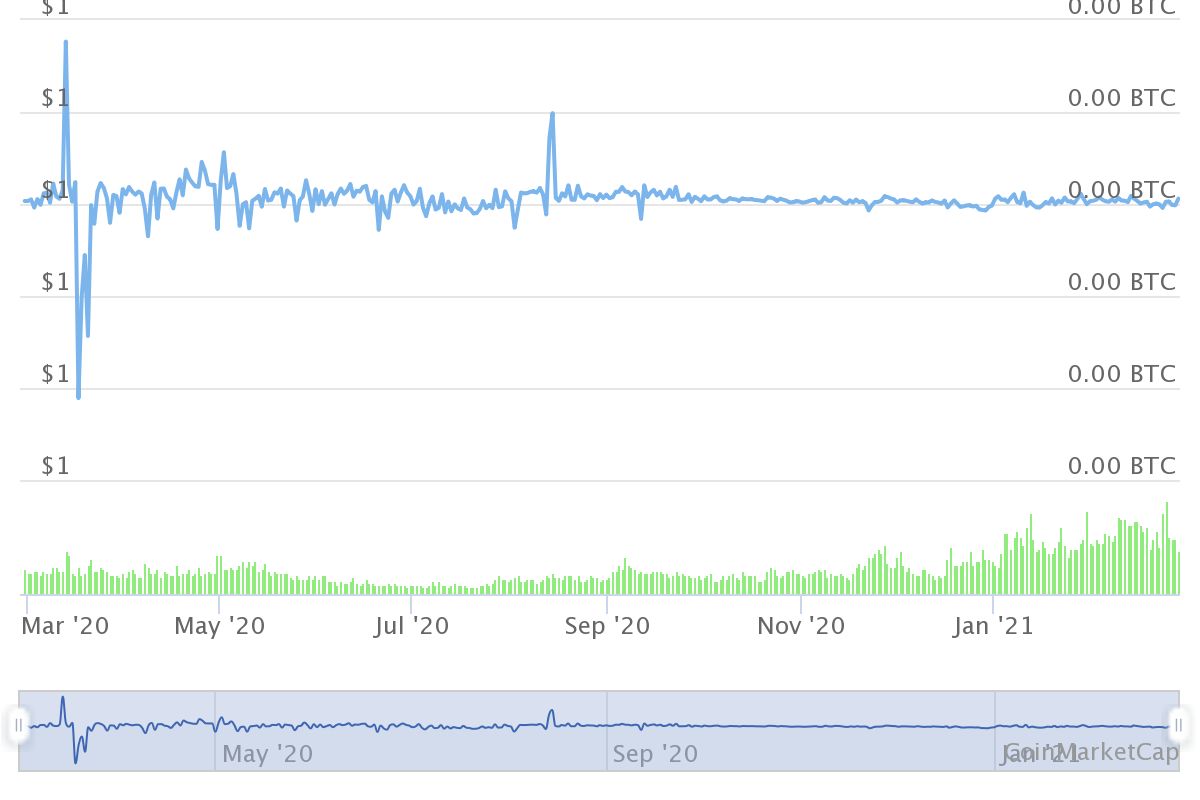

This piece is especially important in the context of the ongoing sharp rise in the dollar price of bitcoin. As bitcoin and cryptocurrency gains even more mainstream awareness and institutional acceptance, one must ask how much of this rise is pure speculation and how much is an educated guess about the future of assets & capital in general. The article lays out Winklevoss Capital’s case against the current liquidity boom fulled by relentless currency printing:

Even before COVID-19, and despite the longest bull run in U.S. economic history, the government was spending money like a drunken sailor, cutting taxes like Crazy Eddie, and printing money like a banana republic.

What began as a shot in the arm during the credit crisis of 2008, never stopped, despite the U.S. economy being out of the woods for years. And so what started as an acute prescription, has morphed into chronic dependence and denial (aka addiction). The resulting maladaptive behavior is, not surprisingly, very difficult to correct.

… if stock market gains are your measure of success, you will choose not to upset the apple cart, even if it’s wildly untethered to reality.

The Winklevosses have been early and big believers in cryptocurrency, and have historically held large amounts of it. They also set up the cryptocurrency exchange Gemini which received New York state’s “bitlicense” to operate.